Blog

Blog

10 Questions with Niv Hanan, Business Development Manager

Learn More

September, 2023

Carbon Credits 101

July 2023 registered as the warmest month globally in the last 120,000 years. (1) This is a harsh reminder of our rapidly changing climate and the pressing need for solutions that not only mitigate but actively reverse the environmental damage done.

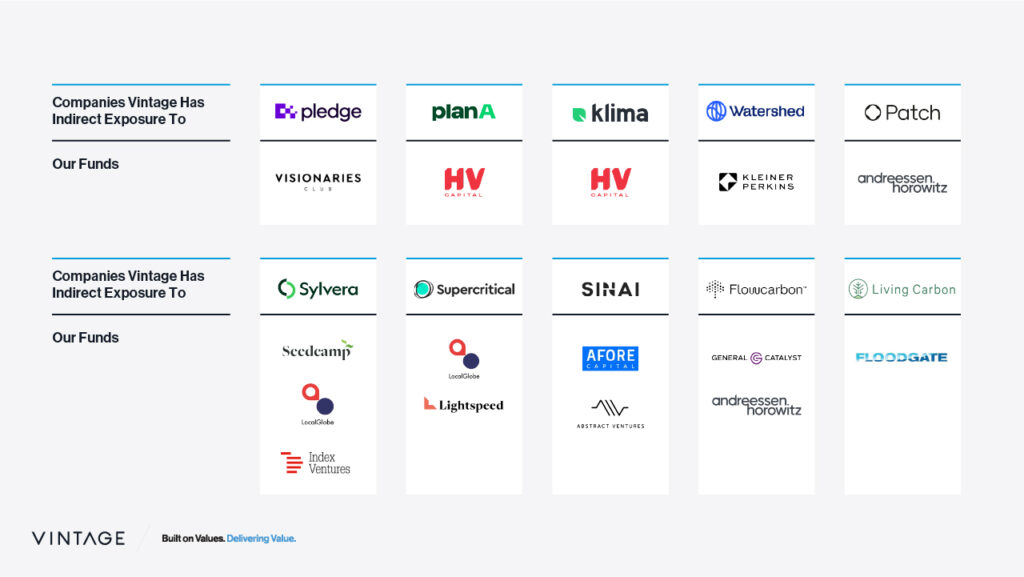

Our previous blog post focused on the overlap between climate and VC. We analyzed our portfolio funds’ investments and developed a framework to understand where funds should “play” in climate.

A standout observation was that the carbon sector, including carbon accounting, avoidance and removal, and voluntary carbon market solutions, is the fastest growing. Carbon companies backed by our funds accounted for only 2% of all climate-related investments before 2020 and more than 15% since 2020.

Below, you can see the carbon companies we have indirect exposure to and where our funds are invested.

Given this undeniable interest, we created a comprehensive 101 guide for the voluntary carbon market, focused on the different types of credits, challenges, and main trends.

Let’s go…

The Need

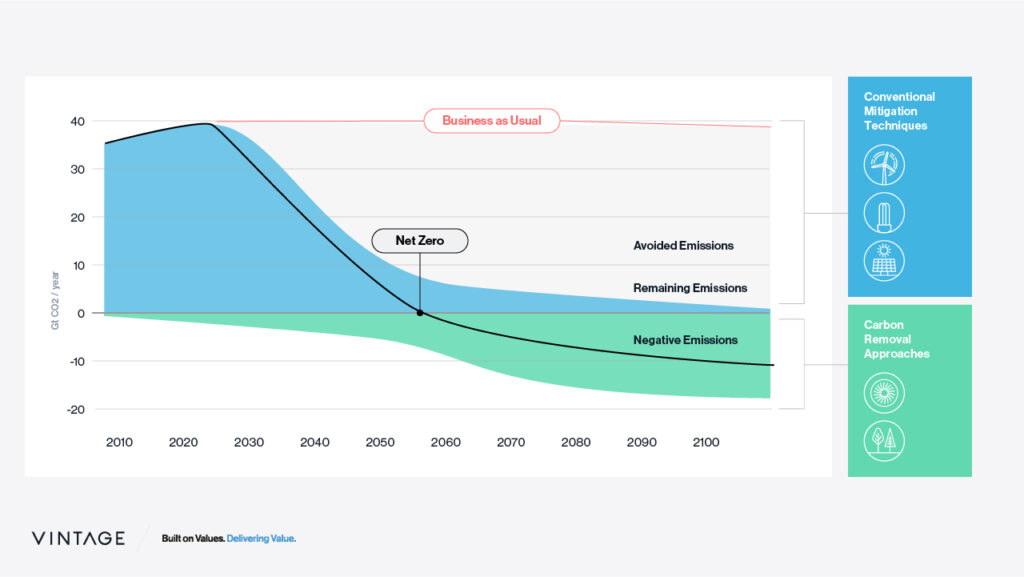

While it has been debated for many years, it’s widely agreed that simply avoiding emissions is not enough. Global warming demands robust carbon removal solutions, and The IPCC estimates that we need to remove 6-10Gt of carbon annually by 2050, but currently, we’re only at 0.003Gt. (2)

A very efficient way to reach the desired goal of carbon reduction at scale is to put a price on carbon. Indeed, governments are doing that through ‘Compliance markets’ using two mechanisms. The first is Carbon Tax – a penalty that businesses pay for their excessive Greenhouse Gas (GHG) emissions (i.e., “polluter pays”). A notable example is the EU’s CBAM, a carbon tax levied on carbon-intensive products imported from non-compliant countries (will enter into application in its transitional phase on 1 October 2023). (3) The second is Cap & Trade via Emissions Trading System (ETS) – “A government regulatory program designed to limit the total level of emissions.” Both mechanisms effectively act as a means for carbon offsetting. However, while Compliance markets are a key contributor to fighting Climate Change, their application remains confined to specific companies in a limited number of countries, and they do not apply to carbon removal.

Private companies that are not bound by carbon taxes or cap and trade mechanisms but want to reach net zero or reduce emissions can offset them through the Voluntary Carbon Markets (VCM). In the VCM, “private actors voluntarily trade carbon credits that represent certified removals or reductions of emissions”. (4)

To move further, we compared the Compliance market and the VCM across key aspects.

Compliance vs. Voluntary Carbon Markets (VCM)

In short, compliance markets are big and effective, regulated, standardized, and relevant today only for avoidance (i.e., no removal). In contrast, the VCM is small, unregulated, based on voluntary commitments, and 20% of credits traded in it are removal credits. Although smaller, VCM’s rapid growth suggests it will play a significant role in future carbon offset efforts.

Compliance markets:

(1) Use Case: used by corporates to trade carbon offsets and to comply with the limits set for them.

(2) Size & Market: nearly 15Gt of CO2e (5) offsets are traded yearly, valued at $850b, the compliance market is significantly larger than the VCM. Growing 2.5x YoY.

(3) Regulation: overseen by governments and international organizations, including the UN. Regulators leading the pack are the EU, China, and California.

(4) Global Context: Global annual emissions hover around 50Gt. The 15Gt in this market is substantial, contributing a major part to combating emissions.

(5) Credit Types: The vast majority of these offsets are ‘avoidance’ rather than ‘removal’. This indicates an imminent need to evolve or adapt financial mechanisms to promote removal credits mechanism.

VCM:

(1) Use Case: The market is entirely voluntary. On the demand side, there are public and private companies that have set voluntary commitments, with many pledging to become ‘net zero’ or carbon negative, like Microsoft. (6) On the supply side, offsets are available thanks to project managers that reduce or remove carbon in multiple ways (e.g., planting trees, Direct Air Capture).

(2) Size & Market: Just a drop in the ocean vs. compliance market. Only 0.5Gt of credits, worth $2b, are traded annually. The VCM is expected to grow from around $2b in 2022 to about $100b in 2030 and around $250b by 2050. (7)

(3) Regulation: Unlike the Compliance market, the certification process is done directly by buyers or by NGOs and is yet to be standardized.

(4) Global Context: There are no geographical constraints to the VCM market. Emissions and credits are treated equally regardless of their source.

(5) Credit Types: Another major difference is that in the VCM ~20% of credits are removal, indicating that the current marketplace for removal credits is the VCM.

How Does Credit Issuance Work in the VCM? (8)

(1) Project Development: After project developers identify and develop projects that reduce emissions or remove them from the atmosphere, a baseline assessment begins, and the baseline level is established by determining expected emissions without the project’s implementation (mostly done for nature-based projects).

(2) Measurement, reporting, and verification (MRV): Once the project is operational, emissions are monitored and verified regularly by independent auditors according to a methodology that is approved by independent scientific advisory boards of third-party certifying bodies. Then, the verified credits are submitted to a carbon credit registry which serves as a database to track the issuance, transfer, and retirement of all credits. After registering, third-party organizations (the certification bodies who approved the methodology) conduct the verification process to ensure the projects’ adherence. Various certification standards exist; some well-known ones include the Gold Standard, (9) Verified Carbon Standard (VCS) by Verra,(10) and Climate Action Reserve (CAR), (11) among others. However, leading buyers often have their own internal teams approving projects.

(3) Trading: Carbon credits can be bought and sold on the VCM once certified.

(4) Retirement: Once the credit is retired from a market, it can no longer be sold or traded. Retiring a credit means it has been purchased, and its value of one ton of CO2 has been reduced from the purchaser’s overall carbon footprint.

While the process varies depending on the specific certification standard or registry, every process should ensure that credits are real, additional, measurable, and verifiable. One of the VCM’s largest challenges is that there is no single clear and widely adopted process.

Since demand for carbon credits by private companies is relatively straightforward and exceeds supply, we focused our research on the supply side, which is much trickier and has a long way to go. We analyzed the different supply types – including the pros and cons for each – and discovered that not all credits are created equal…

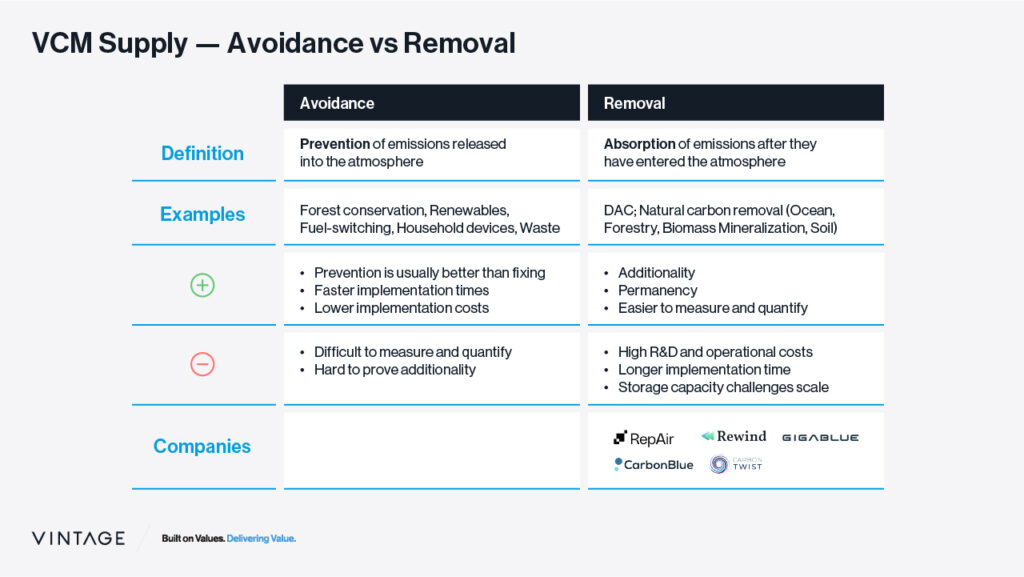

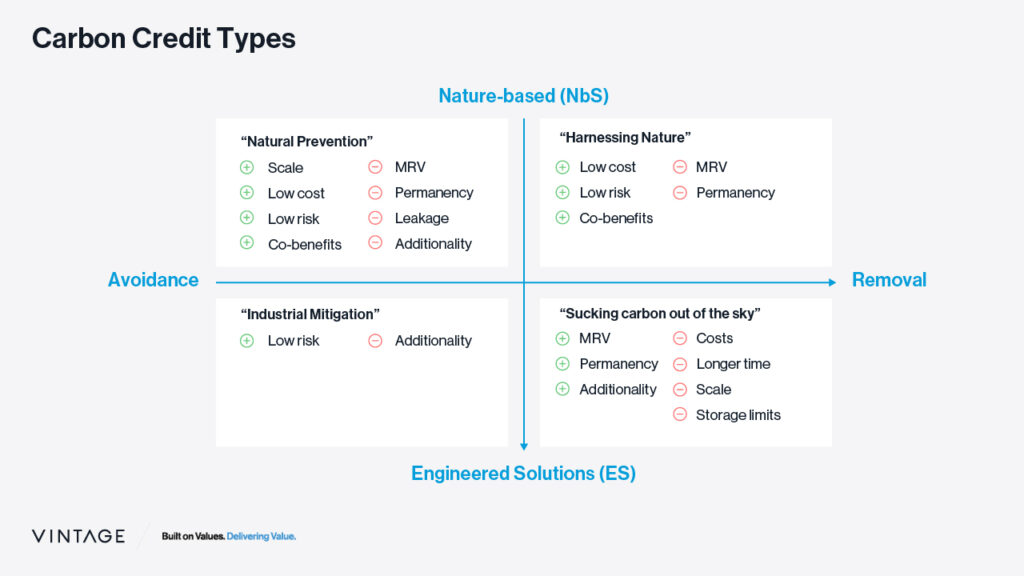

VCM Supply – Avoidance vs Removal

As briefly mentioned, VCM has both avoidance and removal (12) credits. We outlined the pros and cons for each and gave some examples.

Avoidance credits refer to preventing the release of emissions into the atmosphere and are enabled through means such as forest conservation, renewable energy, fuel-switching, efficient household devices, and waste management. The advantages of avoidance credits lie in the fact that prevention is often more effective than trying to fix the damage caused by emissions after it’s done. Additionally, implementing avoidance measures tends to be faster and more cost-effective. Challenges associated with avoidance credits include difficulties in accurately measuring and quantifying avoided emissions (MRV).

Furthermore, proving additionality, which means demonstrating that the avoided emissions are additional to what would have occurred without the project, is often complex.

Removal credits refer to the process of absorbing emissions after they have been released into the atmosphere. These credits are created through technologies such as Direct Air Capture (DAC), ocean carbon sequestration, forestry projects (i.e., planting new trees), biomass mineralization, and soil carbon sequestration. The advantages of removal credits include the concept of additionality, permanency (i.e., keeping carbon off the atmosphere for very long periods, which vary depending on the credit production method (13)), and are generally easier to measure and quantify than avoidance credits. Challenges include high R&D costs, high operational costs, longer timeframes, and storage capacity as the scale of removal efforts increases.

Some of the companies dealing with removal are Rewind, CarbonBlue, and GigaBlue. Rewind (backed by Yes VC, ZORA Ventures) will relocate biomass to the bottom of the Black Sea. CarbonBlue (backed by Jibe Ventures, Fresh.Fund) will remove excess CO2 from seawater and lock it away indefinitely, and by doing so, will counter ocean acidification and enhance the ocean’s ability to absorb more CO2 from the atmosphere. Lastly, GigaBlue (backed by At One Ventures, Fresh.Fund) developed geo-optimized particles that stimulate phytoplankton growth, and then sink into the deep ocean, sequestering carbon for over 1,000 years.

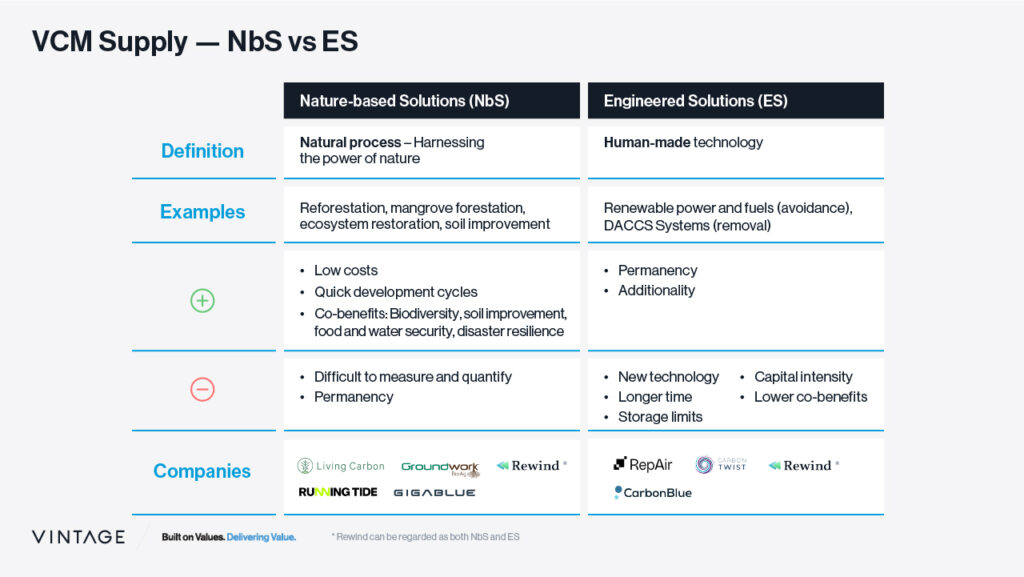

VCM Supply – Nature-Based Solutions (NbS) vs Engineered Solutions (ES)

Another way to distinguish types of carbon credit supply is NbS vs. ES.

Nature-based Solutions (NbS) refer to the utilization of natural processes in reducing or removing emissions. These solutions encompass various methods such as reforestation, mangrove forestation, ecosystem restoration, and soil improvement. NbS offers several advantages, including low costs and quick development cycles, and they provide co-benefits such as enhancing biodiversity, improving soil health, ensuring food and water security, and enhancing disaster resilience. The key challenges of NbS are around MRV, permanency, leakage and additionality. While there is plenty of evidence that most current NbS removal methods have very little impact on Co2 concentrations, this is changing with more permanent and robust solutions, coupled with advanced MRV technologies.

Examples of NbS companies include GroundWork BioAg, Running Tide, and Living Carbon among others. GroundWork (backed by MoreVC, Ibex Ventures) produces mycorrhizal inoculants for mainstream agriculture, which improves plant health and fertility while permanently sequestering carbon. Running Tide (backed by Venrock, Yes VC, Founder Collective, Transition) develops permanent carbon removal solutions through regenerative Aquaculture. Living Carbon (backed by Floodgate, Lowercarbon Capital, Prelude Ventures, Felicis, Homebrew, EQT, Village Global) develops genetically engineered trees that grow faster, bigger, and sequester more carbon. GigaBlue and Rewind, (14) which we mentioned earlier, are also NbS solutions.

Engineered Solutions (ES) involve the use of human-made technologies, primarily to create energy or remove carbon, in a way that couldn’t be achieved naturally. These solutions encompass various approaches, such as renewable energy and fuels (avoidance), and DAC (removal). ES offers some clear benefits, including the potential for permanency and additionality. Challenges include the fact that the development of new technologies is, in most cases, R&D-intensive and involves much longer timeframes. Moreover, in some cases there may be limitations on storage capacity, constraining the scalability of these solutions. Finally, ES tends to have a higher capital intensity and may offer fewer co-benefits than NbS.

Example of ES companies are Carbon Twist and Repair. Carbon Twist (backed by Hetz Ventures, Grove Ventures) is developing a solution that effectively removes methane from the air in various settings, including cow sheds, gas leaks, coal mines, and landfills. RepAir (backed by Extantia, Equinor, Shell Ventures, Zero Carbon Capital) created a DAC system based on proprietary electrochemical cell technology (also regarded as a removal company). A few companies we mentioned earlier – Rewind, (15) and CarbonBlue, are also considered ES solutions.

To make it more transparent and better understand the pros and cons of each credit type, we created a 2×2 matrix that summarizes the different supply types – Avoidance vs. Removal * NbS vs. ES.

VCM Challenges and Critics

Because the VCM is nascent and unregulated, it faces significant challenges and critics, mostly around transparency, credibility, and accessibility, restricting its growth:

(5) Transparency: inconsistent credit quality due to a lack of standardized evaluation criteria is the underlying reason for market opaqueness, making it challenging for buyers to determine the true value of the credits they purchase. In addition, the presence of multiple intermediary functions in the market creates complexities and inefficiencies, increasing transaction costs and making it harder to track backward the impact of those credits.

(6) Credibility: the lack of standardized criteria in crucial areas such as MRV and leakage (16) undermines market credibility and raises doubts about the true impact of the purchased credits. This challenge peaked in May 2023 when David Antonioli, the CEO of Verra, the world’s leading carbon credit certifier, announced his resignation amid concerns that the organization approved millions of worthless credits used by major companies. Verra’s carbon standard has faced criticism, with investigations revealing questionable practices related to rainforest credits (i.e., nature-based avoidance credits) used by big corporations such as Disney, Shell, Gucci, and others. This event created deep issues that led some firms to move away from their commitments – Gucci removed a carbon neutrality claim from its website after heavily relying on Verra’s carbon credits. (17)

(7) Accessibility: barriers to trading. On the supply side, onboarding registered and certified credits on the platform is difficult. This process is not structured and varies across projects, involves different standards, takes a relatively long time, and is often very expensive (hurting the project’s unit economics). On the demand side, it’s almost impossible for individuals to participate and very complex for companies because of the lack of price transparency, quality uncertainties, and relatively low trading volume.

(8) Greenwashing and a substitute for emissions reduction: the current voluntary market “operates in the shadows,” with some good “but lots of bad” in the system, says former Bank of England governor Mark Carney, now UN special envoy on climate action and finance. Because the market is voluntary, there is no regulation on price or quality, and companies (buyers) aren’t required to disclose this information, there is a lot of room for manipulation. Such manipulations might include ‘greenwashing’ and ‘license to pollute.’ Companies with deep pockets might find it beneficial to increase their carbon footprint while buying cheap, low-quality credits. This way, the company will claim it has reduced emissions while, in reality, emissions are externalized.

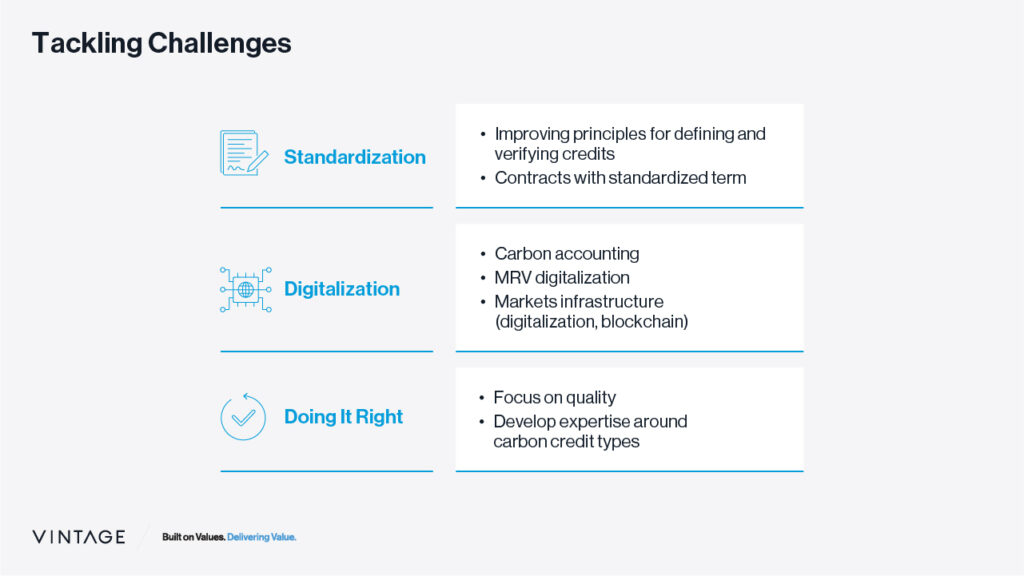

Tackling Challenges

Fundamental changes are needed if the VCM is to grow and become a meaningful part of the solution. We bucketed them into three groups which we believe are catalysts to allow healthy growth:

(1) Standardization: align on principles for defining and verifying credits by standard. Standardization is critical to overcoming most credibility issues and some transparency issues. While this is mostly an issue of policy and regulation, we see more and more digital quality enablers popping up. One is Sylvera (backed by LocalGlobe, Index, Seedcamp, Insight), a carbon offset ratings platform that makes offset quality and risks transparent for all parts of the value chain – sellers, intermediaries, buyers, and investors. Another company is Patch (backed by a16z, Coatue, GIC), which builds infrastructure for the carbon markets by connecting companies to vetted climate action projects across various technologies and geographies. Some efforts in the right direction are being made. In June, (18) the Voluntary Carbon Markets Integrity (VCMI) introduced new standards for transparency and MRV issues in the VCM. (19) These include guidelines for corporate buyers and a measure of credit reliability.

(2) Digitalization: the shift from manual to digital, making the market more efficient and scalable. This includes carbon accounting, MRV for carbon projects, and market infrastructure. Digital carbon accounting platforms are helping organizations become smarter on their carbon math in a much more efficient and scalable way; Digitalized MRV processes (e.g., using satellites to measure tree growth instead of people) are improving credits’ credibility and allow for better, faster, and cheaper techniques for project managers to get certified credits. Digitalization of markets such as digital marketplaces and blockchain solutions is solving transparency and accessibility issues. One of the famous companies in the space is Watershed (backed by Kleiner Perkins, Sequoia, Transition), an enterprise climate platform for companies to measure, report, and act on their carbon emissions. Another company is Flowcarbon (backed by a16z, General Catalyst, BoxGroup), which brings carbon credits onto the blockchain. An Israeli example is Albo Climate (backed by Techstars and Microsoft AI for Good Accelerator) which leverages AI and satellite-powered technology for remote sensing and monitoring nature-based (NbS) carbon removal.

(3) ‘Doing it right’: Following the Verra incident and alike, buyers and sellers are seeking higher quality credits that are moving the needle on climate change. More and more corporates (demand) and project managers (supply) develop expertise around carbon credit types and strategies accordingly.

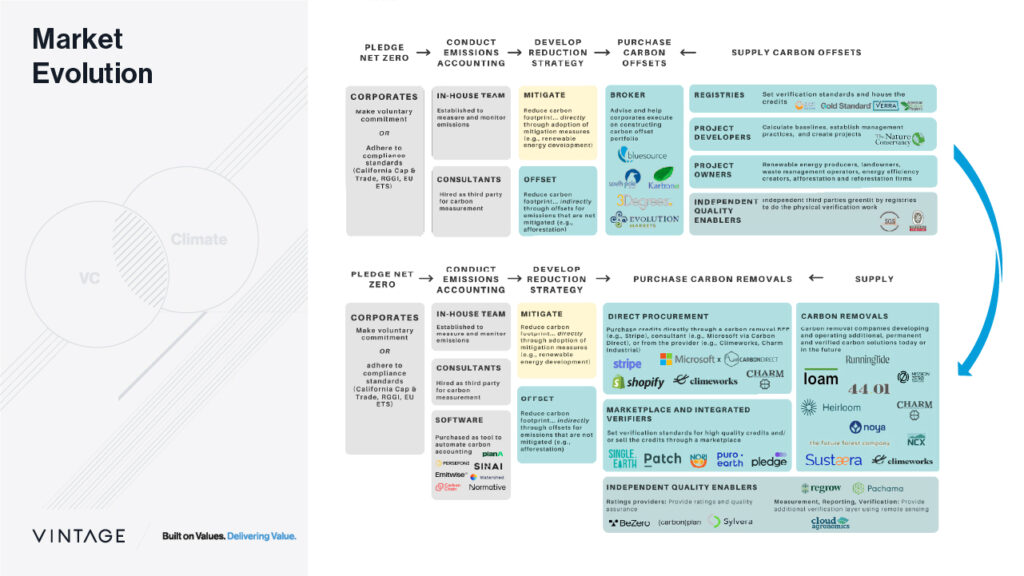

Standardization, Digitalization, and More – Market Evolvement

The slide below, based on CTVC’s publications, (20) demonstrates the change that the market is undergoing in each of the buckets highlighted above – the emergence of carbon accounting platforms (today a red ocean), direct credit procurement solutions and marketplaces, quality enablers, and verifiers, and finally – carbon removal technologies.

Doing it right – the demand side

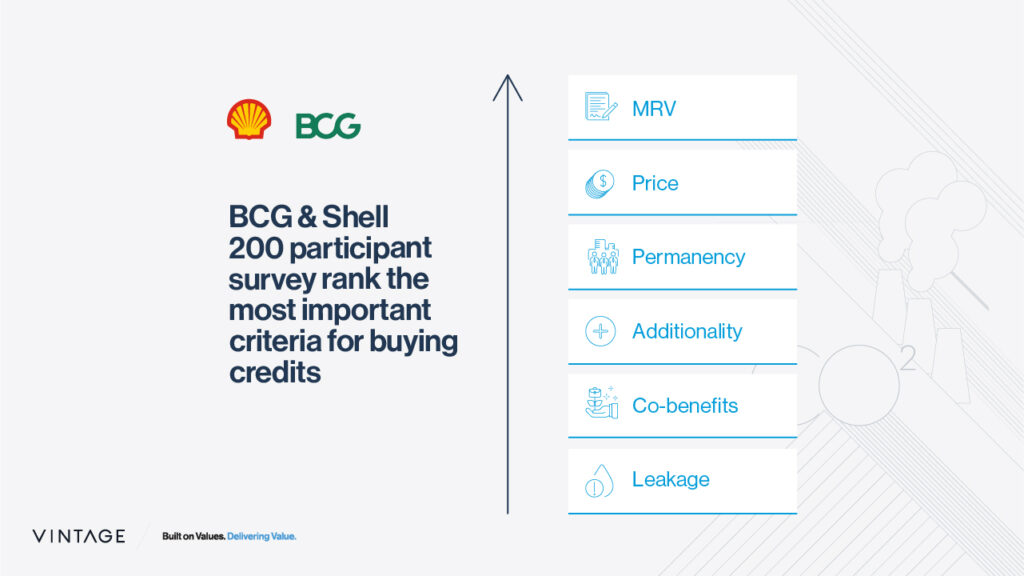

A “BCG & Shell” 200-participant survey ranked the most important criteria for buying credits: MRV, Price, Permanency, Additionality, Co-benefits, and Leakage. “91% of buyers rank MRV as one of the top three most important quality criteria for their purchases. Buyers want to ensure their credits have a measurable benefit, with concerns over the reputational impact of buying ineffective credits”(21). We conducted a similar survey among 18 generalist VCs from our local industry, and we received similar results: MRV and Price were the most important. We see an increasing trend – companies want legit credits with clear benefits and are willing to pay higher.

Ending Note:

The world is heating up, and the time to act is now – businesses and governments are looking for technologies that will help reduce and remove emissions at scale and support the surrounding ecosystem. Just recently, it was reported that the Biden administration bet $1.2 billion on giant carbon-sucking vacuums that will be placed in Texas and Louisiana and will become a global testing ground as a potential climate solution. (22) There is a growing understanding that voluntary commitments are meaningful, and that removal is a must, but at the same time, there is no supportive regulation and standardization mechanisms. In this complex and uncertain environment, the VCM has flourished.

While it’s pretty clear that a massive new carbon industry will be built in the coming decades, it’s risky to build and invest today in businesses solely based on carbon credits in the VCM. Until we see more regulation and standardization processes introduced, and because we are long-term believers in the space, we recommend players to:

References

[1]https://news.un.org/en/story/2023/08/1139527#:~:text=The%20global%20average%20temperature%20for,and%20partners%20said%20on%20Tuesday.

[2] https://www.carbon-direct.com/research-and-reports/state-of-the-voluntary-carbon-market

[3] https://taxation-customs.ec.europa.eu/carbon-border-adjustment-mechanism_en#key-elements

[4] https://climatefocus.com/so-what-voluntary-carbon-market-exactly/

[5] Carbon dioxide equivalent or CO2e means the number of metric tons of CO2 emissions with the same global warming potential as one metric ton of another greenhouse gas and is calculated using Equation A-1 in 40 CFR Part 98 (United States Environmental Protection Agency).

[6] https://blogs.microsoft.com/blog/2020/01/16/microsoft-will-be-carbon-negative-by-2030/

[7] https://www.morganstanley.com/ideas/carbon-offset-market-growth#:~:text=With%203%2C800%20more%20projects%20listed,around%20%24250%20billion%20by%202050

[8] The Voluntary Carbon Market Explained by VCM Primer: https://vcmprimer.org/

[9] https://www.goldstandard.org/

[10] https://verra.org/programs/verified-carbon-standard/

[11] https://www.climateactionreserve.org/

[12] For elaboration: Business Braekdowns” podcast episode – Carbon Removal: A Primer (

[13] https://roberthoglund.medium.com/carbon-can-be-temporarily-stored-for-a-long-time-4bd7f94e3156

[14] Rewind can be regarded as both NbS and ES

[15] See note 13

[16] Unintended increase in emissions in one area as a result of emission reduction efforts in another area

[17] https://www.theguardian.com/environment/2023/may/23/ceo-of-worlds-biggest-carbon-credit-provider-says-he-is-resigning

[18] https://www.reuters.com/sustainability/climate-energy/global-initiative-launched-rate-corporate-carbon-offset-claims-2023-06-28/?ref=ctvc.co

[19] https://vcmintegrity.org/vcmi-claims-code-of-practice/?ref=ctvc.co

[20] https://www.ctvc.co/giving-carbon-credit-where-its-due/

[21] A report by Shell and BCG: The voluntary carbon market: 2022 insights and trends

[22] https://www.washingtonpost.com/business/2023/08/11/carbon-capture-vacuum-biden/

Get in touch with Lior Elovitch:

Share